CASE STUDY: Customer-Driven KPIs for a Billing Process

by Stacey Barr |This case study is a process definition for a Billing Process, adapted from a real freight business. It shows the steps for not only improving a business process, but using the process to identify both Process Result and In-Process measures.

Using rail as their primary mode, the freight business featured in this case study hauled bulk freight, such as grain or livestock, for their customers.

Their performance measurement challenge

Via their customer survey, the freight business identified that one of the top three priorities for improvement was the accuracy of their billing process. Customers were not paying bills because they were based on inaccurate or confusing rates.

The challenge was to measure and improve three specific performance results:

- timely payment of invoices

- revenue collected for all consignments handled

- ease of understanding of invoices, statements and adjustment notes

How they overcame these challenges

A small team from the freight business worked together, using PuMP, to:

- Define their billing process and its purpose.

- Analyse their billing process to identify where the causes of problems were.

- Develop performance measures to monitor the improvement of the billing process.

Here’s what they did…

Process Result Measures:

Measures of the above three performance results were called ‘Process Result Measures’. The team decided on six:

- Value of Overdue Accounts = The total amount of revenue currently outstanding for accounts that have not been paid by their due date.

- Lateness of Overdue Accounts = The average number of days that overdue accounts are overdue by.

- % Freight Movements Billed = The total number of freight movements (consignments) that have been billed as a percentage of the total number of freight movements that have been consigned.

- Customer Satisfaction with Invoice Accuracy = The average satisfaction rating provided by customers about the accuracy of invoices they receive from us.

- Bad Debts as a % of Revenue = The total amount of revenue for invoices classified as bad debts, as a percentage of the total amount of revenue received.

- Cost of Billing = The total labour costs associated with preparing, sending and following up invoices.

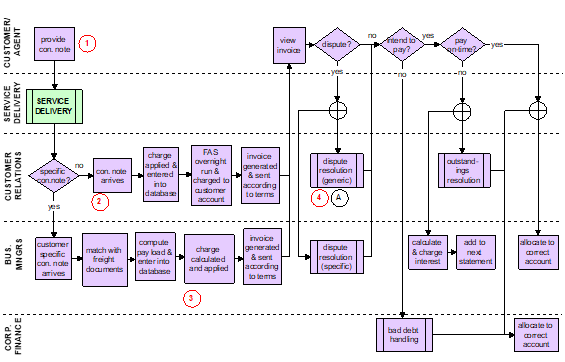

The Process Flowchart and problem areas:

To understand how the billing process might be improved, to improve performance as defined by their six Process Result Measures, the team created a process map:

Process Problem areas:

After mapping the billing process, the team systematically stepped through it to identify the problems that currently prevented good performance in the Process Result Measures:

- Freight consignment notes are not always supplied when they should be, and freight is shipped without them.

- Freight consignment notes go missing when they are paper-based.

- The wrong charges can be applied when the data about exactly what freight and what amount of freight is not accurately provided by the customer.

- Accounts should never get to this stage, but there is a considerable number that are in dispute over what has been invoiced and the charges applied.

In-Process Measures:

Before they decided how to fix these billing process problems, the team designed a few measures to track these problems, so they could tell whether or not their fixes were working. They called these measures ‘In-Process Measures’:

- % Freight Consignment Notes Not Supplied = The number of consignments where a consignment note was not supplied as a percentage of the total number of consignments.

- % Freight Consignment Notes Electronic = The number of consignment notes that were supplied electronically as a percentage of the total number of consignment notes supplied.

- Accuracy of Freight Data = Number of errors found in quantity or type of freight that would affect how the freight was charged, divided by the number of freight consignments.

- Value of Accounts in Dispute = The total amount of revenue associated with accounts that are currently being disputed by customers.

With this collection of six result measures and four in-process measures, the team could focus very directly on fixing the problems that mattered most, and making sure that their efforts were improving the in-process measures, and in turn improving the process result measures.

TAKE ACTION: Where can you use process analysis – including identification of process measures – to help you improve a strategic outcome or goal?

Join Measure Up

Sign up for the Measure Up newsletter and get free access to the "10 Secrets to KPI Success" online course and e-book.

Upcoming KPI Training

All our PuMP training options have moved to PuMP Academy.

Connect with Stacey

Haven’t found what you’re looking for? Want more information? Fill out the form below and I’ll get in touch with you as soon as possible.

167 Eagle Street,

Brisbane Qld 4000,

Australia

ACN: 129953635

Director: Stacey Barr